Golden Dome Contractors: Who's Actually Building the $185B Space Shield

On Friday, April 24, 2026, U.S. Space Systems Command (SSC) lifted the curtain on the most consequential prototype competition in American missile defense since the demise of Reagan-era "Star Wars." Twenty Other Transaction Authority (OTA) agreements — collectively worth up to $3.2 billion — had quietly been signed in late 2025 and early 2026 with twelve companies to design and demonstrate space-based interceptor (SBI) prototypes for the Golden Dome architecture. The full list became public only that morning.

The twelve names: Anduril Industries, Booz Allen Hamilton, General Dynamics Mission Systems, GITAI USA, Lockheed Martin, Northrop Grumman, Quindar, Raytheon (RTX), Sci-Tec, SpaceX, True Anomaly, and Turion Space. A roster that, taken together, reads like a stress test of the post-2020 defense industrial base: three legacy primes, two integrators, one orbital launcher with a side hustle, one autonomy unicorn, and five startups whose collective age is younger than the F-35 program.

Demonstration deadline: 2028. Total program ceiling, all components, all phases, through 2035: $185 billion. And the man running it, Space Force Vice Chief Gen. Michael Guetlein, has already told Congress that the SBI piece may not survive contact with reality.

This is a guide to the twelve. What each one is building. What heritage they bring. What's at stake if the architecture descopes — and who is best positioned for the long-cycle win.

The April 24 Announcement: What SSC Actually Said

Confirmed: Twelve companies, twenty OTA agreements, up to $3.2 billion ceiling value, with a directive to demonstrate "an initial capability" integrated into Golden Dome by 2028. The architecture envisages a proliferated LEO constellation capable of engaging missiles in boost, midcourse, and glide phases.

Concealed: Individual award amounts, the specific role assigned to each vendor, and the technical architecture of any prototype. SSC cited operational security. What follows synthesizes each contractor's existing program portfolio, recent press disclosures, and executive statements after the announcement. For broader context, see our Golden Dome arms race piece and the militarization of space.

The Strategic Question: Can Boost-Phase SBI Actually Work?

Reagan's Strategic Defense Initiative consumed roughly $30 billion (in then-year dollars) over a decade and produced no operational space-based interceptor. SDI collapsed under three problems that have not gone away: cost-per-shot economics, sensor-to-shooter timelines, and the absence number — the math of how many on-orbit interceptors must be in the right plane at the right time to engage even one boosting ICBM.

What's different in 2026 is the smallsat industrial base. A Falcon 9 puts ~22.8 metric tons into LEO for under $70 million; SpaceX builds and deploys hundreds of satellites per year on the Starlink line. Anduril has flight-proven software that fuses distributed sensor data on autonomous platforms in seconds. AI-driven target track and engagement decision logic is no longer notional.

But Gen. Guetlein, testifying on April 15 before the House Armed Services Subcommittee on Strategic Forces, refused to oversell what is now being designed: "If boost-phase intercept from space is not affordable and scalable, we will not produce it because we have other options to get after it." And: "What we do not know today is, can I do it at scale, and can I do it affordably?"

That caveat tells program managers and investors exactly where the descope risk lives. The sensor layer (PWSA Tranche 3, Next-Gen OPIR), the C2 software layer (Anduril/Palantir), and the ground-based midcourse and terminal layers (NGI, THAAD, SM-3, Patriot) are nearly certain to survive any budget cut. The space-based kinetic interceptor — a satellite that releases a hit-to-kill vehicle to ram a boosting missile — is the piece most exposed.

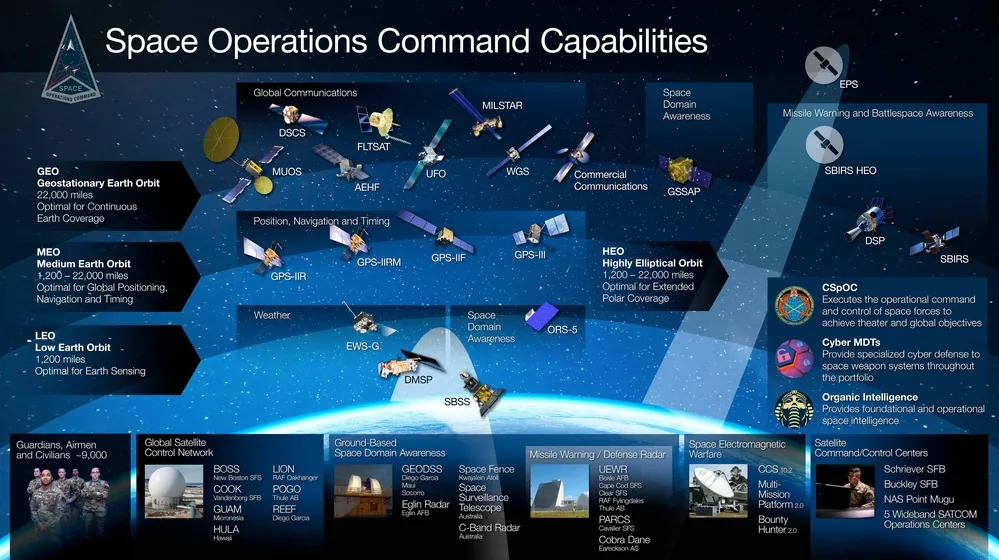

The Architecture: Where SBI Sits in Golden Dome

Golden Dome is not one weapon. It is a system of systems layered across four kill chains.

| Layer | Function | Lead Programs | Prime Contractors |

|---|---|---|---|

| Sensor (Space) | Missile warning, tracking, targeting | PWSA Tranche 3 ($3.5B); Next-Gen OPIR; Resilient MWT-MEO | Lockheed Martin, L3Harris, Rocket Lab, Northrop Grumman |

| Sensor (Ground/Sea) | Target discrimination, fire control radar | Long Range Discrimination Radar (LRDR); SPY-6 | Lockheed, Raytheon |

| C2 / Battle Management | Sensor fusion, AI target prioritization | Anduril Lattice + Palantir Foundry integration | Anduril, Palantir |

| Communications / Mesh | Encrypted, jam-resistant data transport | MILNET (480 sats), Space Data Network ($1.6B FY27 ask) | SpaceX |

| Interceptor (Boost-phase, Space) | LEO kinetic kill of boosting ICBMs | SBI Prototype Program ($3.2B OTA) | The 12 named here |

| Interceptor (Midcourse) | Exoatmospheric kill in midcourse phase | NGI, GMD upgrades, SM-3 Block IIA | Lockheed (NGI), Raytheon (SM-3) |

| Interceptor (Glide-phase) | Hypersonic glide vehicle defeat | GPI (US-Japan) | Raytheon, Northrop |

| Interceptor (Terminal) | Last-chance defeat | THAAD, Patriot PAC-3 | Lockheed |

In FY27 the Pentagon is asking for $17.9 billion for Golden Dome — but ~$17 billion of that sits in not-yet-approved reconciliation funding rather than the base budget. Reconciliation is contingent on legislation that has not yet passed. The $6.4 billion in FY27 RDT&E for the three big space-based missile-warning programs (Next-Gen OPIR, Resilient MWT-MEO, SDA Tracking Layer) is real and largely funded; the SBI prototype dollars sit in the more uncertain pile.

Golden Dome's space-based interceptors will sit on top of this existing capability stack — layered above the SDA Tracking Layer, the Space Data Network, and the GBI/THAAD/SM-3 ground-based defense in depth.

The Primes: Heritage Incumbents, Heritage Risks

Lockheed Martin (NYSE: LMT)

Lockheed is the prime with the most to gain and the least to lose. Its Missiles and Fire Control segment already builds THAAD, is plant-tooling to quadruple THAAD output and triple PAC-3 production, and is the prime on the Next Generation Interceptor (NGI) for ground-based midcourse — driving toward a 2029 first flight. Lockheed Space won an SDA Tranche 3 Tracking Layer slice (~$1.1 billion for 18 satellites) and continues to deliver Next-Gen OPIR missile warning satellites.

For SBI, Lockheed's most credible proposal is an interceptor satellite drawing on the NGI kill-vehicle heritage plus the bus and propulsion experience of A2100 and LM 400. Lockheed has the integration muscle to do all of it — interceptor, sensor, C2 — and is already inside almost every adjacent kill chain. Risk: fixed-price pressure is shrinking Lockheed's cost-plus comfort zone. Full segment portrait in our Lockheed Martin Space deep dive.

Northrop Grumman (NYSE: NOC)

Northrop has been the most public Golden Dome bidder. The company has confirmed it is ground-testing space-based interceptor prototypes, is offering its Integrated Battle Command System (IBCS) as the cross-service C2 backbone, and is doubling solid rocket motor capacity from 13,000 units in 2024 to 25,000 by 2029. Its Tranche 3 slice ($764M for 18 satellites) gives it sensor presence; Sentinel and B-21 provide the strategic-deterrent credibility to carry an interceptor program politically.

Industry consensus has Northrop offering a rocket-powered kinetic kill vehicle on a Northrop-built bus, drawing on OmegA motor heritage and GMD kill-vehicle work. See our Northrop Grumman Space deep dive. Risk: Northrop's bid is the most direct kinetic play; if boost-phase descopes, its interceptor revenue shrinks more than its sensor and motor revenue.

Raytheon (NYSE: RTX)

Raytheon brings the deepest interceptor heritage on the list — SM-3 (the only U.S. interceptor with an exoatmospheric kill record), SM-6, Patriot PAC-3, and the Glide Phase Interceptor (GPI) with Japan, mandated to IOC by end-2029. RTX has invested heavily in seekers and divert-and-attitude-control systems — both directly applicable to space-based hit-to-kill.

Raytheon's most likely SBI contribution: kill-vehicle architecture, IR seeker subsystems, and possibly a complete interceptor concept reusing SM-3 Block IIA components in a satellite-launched configuration. The challenge is mass — SM-3 Block IIA is ~1,500 kg at launch; an orbital variant must shrink dramatically. Risk: RTX's commercial-aviation exposure (Pratt & Whitney, Collins) makes SBI a smaller revenue lever than for pure-play defense peers — but that diversification also cushions any descope.

General Dynamics Mission Systems (NYSE: GD)

GD is the quiet, classified-heavy prime here. GD Mission Systems specializes in space and ground C2 hardware, secure communications terminals, and signals processing for the IC and DoD. The most plausible SBI role: secure communications and ground operations infrastructure rather than the interceptor satellite itself. Risk: Low. Encrypted comms and ground ops are required regardless of whether the interceptor flies in space or from a silo.

Booz Allen Hamilton (NYSE: BAH)

The only pure integrator on the list. Booz Allen has expanded aggressively into AI/ML and defense-systems integration via Booz Allen Ventures (also a Quindar investor — a relationship presumably cleared with SSC's contracting office). Likely contribution: systems engineering, integration, modeling-and-simulation, and digital engineering twins for the proliferated SBI architecture. Risk: Like GD, descope-resistant — every Golden Dome variant needs systems engineering.

The New Space Disruptors

SpaceX

SpaceX is the only firm on this list that simultaneously builds satellites at industrial scale, launches them, operates them, and writes the autonomy software that flies them. The April 28 disclosure of a planned Space Data Network ($1.6 billion FY27 reconciliation ask) makes SpaceX even more central to the Golden Dome data fabric.

For SBI, the natural play is a Starshield-derived interceptor bus — production-line economics of Starlink, hardened for the military mission, with a divert/kinetic-kill payload. Whether SpaceX or a partner (such as Anduril) builds the kill vehicle is unclear. The previously reported $2B Starshield missile-tracking constellation already provides a built-in sensor layer for any SBI fire-control loop. Position: Strongest of the twelve. Even if boost-phase SBI descopes, SpaceX wins everywhere else in Golden Dome.

Anduril Industries (private)

Anduril is the autonomy and edge-AI prime of this generation. Lattice is the leading C2 backbone for distributed unmanned systems and is being integrated with Palantir's Foundry to form the Golden Dome battle-management core. In April 2026 Anduril disclosed it would build a highly maneuverable satellite carrying a long-wave infrared sensor and a Lattice-based mission data processor — explicitly tied to boost-phase missile detection. The company is also partnering with Impulse Space on an in-space mobility stage that could plausibly serve as an interceptor kick stage. Anduril's March 2026 acquisition of ExoAnalytic Solutions (the leading commercial SDA optical network) further consolidates its sensor-data position.

Position: Anduril sits at three layers — LWIR sat, Lattice C2, and SDA. Even if no kinetic interceptor flies, Anduril's C2 role is locked in. Private valuation reported at ~$30B in late-2024 rounds; an IPO has long been rumored.

The Startups: Why They Were Selected

The most surprising names on the list are the five venture-backed startups. Their inclusion is a deliberate Pentagon signal: SBI procurement will be run through the new-space playbook, not the traditional FAR-based prime contracting model. The OTA structure exists precisely to let early-stage companies compete without three-year proposal cycles.

Rocket Lab is one of the 12 Golden Dome SBI prototype contractors and one of four primes also building the SDA Tranche 3 Tracking Layer — a sign of how the same companies straddle both the sensor and shooter sides of the architecture. Whether boost-phase interception is solvable is open; whether the bus, bus-ops, and ground-software pieces survive is not.

Rocket Lab is one of the 12 Golden Dome SBI prototype contractors and one of four primes also building the SDA Tranche 3 Tracking Layer — a sign of how the same companies straddle both the sensor and shooter sides of the architecture. Whether boost-phase interception is solvable is open; whether the bus, bus-ops, and ground-software pieces survive is not.

True Anomaly (private — $2.2B valuation)

True Anomaly is the purest play on this list. Founded in 2022, the Colorado company makes Jackal, an autonomous orbital satellite designed for rendezvous and proximity operations (RPO) — exactly the maneuvering profile required for any space-to-space engagement — plus Mosaic, its autonomy software platform.

On April 28, 2026, four days after the Golden Dome announcement, True Anomaly closed a $650M Series D at a $2.2B valuation, co-led by Eclipse and Riot Ventures, with Paradigm, Atreides, G Squared, The Private Shares Fund, and VanEck participating. Total raised: ~$1B since 2023 (A $17M, B $100M, C $260M, D $650M, plus $50M Stifel debt). The only startup on this list exclusively focused on orbital defense. Position: Highest pure-play upside — and highest descope risk. If boost-phase dies, the core thesis is wounded.

Turion Space (private)

Founded in 2020 in Irvine, California, Turion operates the DROID family of inspection and SDA satellites. DROID.001 and DROID.002 are on orbit and have delivered more than 40,000 non-Earth-imaging (NEI) frames. Turion has booked 28 U.S. government contracts across NASA, Space Force, SDA, and NRO. In April 2026 the company closed a $75M+ Series B led by Washington Harbour Partners. Its STARFIRE OS is positioned as a multi-mission spacecraft control stack from LEO to GEO.

Position: Turion's likely SBI role is SDA and on-orbit inspection — characterizing adversary objects, providing custody-of-target data — rather than the interceptor itself. Among the most descope-resistant of the startups; SDA grows in any Golden Dome architecture.

GITAI USA

A Tokyo-origin, Los Angeles-based robotics company building autonomous robotic arms and rovers for in-space servicing, assembly, and manufacturing (ISAM). The natural SBI role: robotic on-orbit servicing of interceptor satellites, robotic refueling, or assembly of larger structures from launched components. Position: Speculative but signal-rich. SSC is taking ISAM-enabled sustainment seriously. If boost-phase descopes, the robotic-servicing thesis still maps to PWSA refueling and sensor swap-out.

Quindar

Denver-based mission-control software vendor automating the spacecraft lifecycle from planning through commanding. Founded in 2022 by ex-OneWeb engineers Nate Hamet and Sandilya Bhagavathula. $18M Series A closed November 2025, led by Washington Harbour Partners with Booz Allen Ventures, FUSE, FCVC, and Y Combinator. Capital funds a classified ops facility in the Denver metro. Position: Almost certainly ground operations and mission-management software for the SBI constellation — high-cadence flight ops automation. Software-only, descope-resistant, capital-efficient. The lowest-risk venture position in the cohort.

Sci-Tec

Non-traditional defense small business in Princeton, New Jersey, specializing in mission data processing, missile-warning algorithms, and C2 software. Existing Space Force work includes a $272M data-analytics contract and a $45.8M task order on the Future Operationally Resilient Ground Evolution (FORGE) program for next-generation SBIRS-replacement processing. Position: The algorithm and processing IP layer of SBI. Survives any descope — mission data processing is needed regardless of whether the kinetic interceptor flies. Sci-Tec was reported in early 2025 to be in acquisition talks with Firefly Aerospace; if completed, the competitive landscape shifts meaningfully.

The Twelve in One Table

| Company | Type | Ticker / Stage | Likely SBI Role | Heritage | Descope Resistance |

|---|---|---|---|---|---|

| Lockheed Martin | Prime | NYSE: LMT | Interceptor sat + sensor + integration | THAAD, NGI, GMD KV, A2100 | Medium-high |

| Northrop Grumman | Prime | NYSE: NOC | Kinetic kill vehicle + IBCS C2 + motors | OmegA, Sentinel, GMD KV | Medium |

| Raytheon (RTX) | Prime | NYSE: RTX | Kill vehicle + IR seeker + GPI | SM-3, Patriot, GPI | Medium-high |

| General Dynamics | Prime | NYSE: GD | Secure comms + ground ops | Mission Systems classified | High |

| Booz Allen Hamilton | Integrator | NYSE: BAH | Systems engineering + M&S | Defense IT, AI/ML | High |

| SpaceX | New Space | Private (~$350B) | Bus + launch + data network | Starshield, Starlink, F9/FH | Very high |

| Anduril | New Space | Private (~$30B) | LWIR sensor sat + Lattice C2 | Lattice, ExoAnalytic | Very high |

| True Anomaly | Startup | Private ($2.2B) | Jackal interceptor + Mosaic autonomy | Jackal RPO, Mosaic | Low-medium |

| Turion Space | Startup | Private | SDA + inspection + STARFIRE OS | DROID.001/.002, NEI | High |

| GITAI USA | Startup | Private | Robotic ISAM / servicing | Robotic arms, ISS demos | Medium |

| Quindar | Startup | Private | Mission control software | OneWeb ops heritage | Very high |

| Sci-Tec | Small Business | Private | Mission data processing + algorithms | FORGE, MDPAP, SBIRS | Very high |

Investment Implications

For the public equities, the realistic SBI revenue contribution is a single-digit percentage of total revenue at peak — even for the most exposed primes. Lockheed's Space + Missiles and Fire Control segments together are ~$25B; an SBI prototype slice of $400-600M is meaningful at the segment level but rounds to under 1% of corporate revenue. Northrop is similar. RTX is diluted by Pratt & Whitney and Collins. The real upside is not the prototype itself but the architecture pull-through — whoever wins the prototype phase is positioned for the production phase post-2028. For broader context, see our NASA & DoD space contracts investor guide and space-defense crossover investing guide.

For the private startups, valuation impact has already been priced in part. True Anomaly's $2.2B valuation was pre-funded on the SBI thesis. Turion's $75M+ Series B rode the same wave. Quindar's $18M Series A is conservatively priced and has the cleanest software-margins business. Anduril's eventual IPO — long anticipated — would be the largest single liquidity event in defense tech.

The Likely Descope: Who Survives

Take Gen. Guetlein at his word. Three scenarios are plausible by FY28-30:

Scenario 1 — Full SBI Production. Boost-phase SBI demonstrates and proceeds to production. Total program: $40-80B over a decade. Winners: SpaceX (bus + launch + data), Lockheed and Northrop (interceptor sats), Anduril (sensor + C2), True Anomaly. Sci-Tec and Quindar still win on the ground/processing side.

Scenario 2 — Boost-Phase Descope; Midcourse and Sensor Continue. SSC concludes boost-phase economics don't close. SBI shrinks to a small SDA/midcourse fleet. Winners: Anduril, SpaceX, Turion, Sci-Tec, Quindar, GD, Booz Allen — all the non-kinetic roles. Losers: True Anomaly's pure-play thesis. Lockheed and Northrop pivot capital back to ground-based NGI/GPI.

Scenario 3 — Total Cancellation. Reconciliation funding fails. SBI is folded into the existing PWSA roadmap. The $3.2B prototype ceiling is the floor and the ceiling. Sensor work (Tranche 3, Next-Gen OPIR, MEO MWT) continues; interceptor work essentially stops. Losers: True Anomaly, possibly GITAI and Anduril's interceptor-bus thesis.

The most likely outcome on present facts is Scenario 2. The math of boost-phase intercept from LEO is unforgiving; the math of sensor-layer proliferation is increasingly favorable. The smart money is on contractors whose business survives Scenario 2.

2028 and Beyond

Demonstration deadline 2028. FY27 budget request $17.9B (most of it reconciliation). IOC targeted in the 2030-2032 window for full Golden Dome layered architecture; complete architecture through 2035.

- Late 2026: Prototype critical design reviews. Likely down-select among the twelve — the Pentagon rarely carries 12 OTA awardees intact through a prototype phase.

- 2027: First on-orbit demonstrations. PWSA Tranche 3 launches commence. MILNET reaches full IOC.

- 2028: Integrated SBI demonstration; Pentagon decision on production.

- 2029-2030: NGI first flight (Lockheed); GPI IOC (Raytheon/Northrop with Japan).

- 2030+: Production-phase SBI contracts (Scenarios 1 or 2); full Golden Dome IOC.

Politically, the program crosses two presidential elections (2028, 2032) and at least three defense secretaries. Procurement decisions made between 2027 and 2029 will shape the U.S. national-security space industrial base for the next twenty years.

The Bigger Frame

Golden Dome is the largest single weapons-procurement question facing the United States since the F-35. The F-35 program will ultimately cost more than $2 trillion across its lifecycle. Golden Dome's $185B headline number is an entry ticket to a procurement curve that, on historical missile-defense overruns of 200-400%, could exceed half a trillion dollars by 2040.

Whoever wins the architecture wins the next generation of U.S. defense space. That is why a quiet OTA list — twelve names — mattered enough to be the front-page story for a week. Three legacy primes, two integrators, one launcher-turned-spacecraft-monopolist, one autonomy unicorn, and five venture-backed startups. Some are placeholders. Some are going to be very large companies in 2035. The next two years will sort which is which.

Sources: DefenseScoop, Breaking Defense, SpaceNews, Via Satellite, Air & Space Forces Magazine, Fortune, Bloomberg, CNBC, Aviation Week, The Register, ClearanceJobs, Defense News, Washington Technology, Axios — coverage of the April 24, 2026 SSC announcement and follow-on funding rounds (April 24-30, 2026); Turion Space press release (April 15, 2026); Quindar / SciTec corporate disclosures.