Rocket Lab's $8 Billion Iridium Acquisition, Explained

For most of its two decades, Rocket Lab was the scrappy New Zealand–American company that made a small rocket work when dozens of better-funded startups could not. On June 29, 2026, it announced something no small-launch company had ever attempted: a definitive agreement to acquire Iridium Communications for roughly $8 billion. In a single transaction, a company that still posts annual net losses agreed to buy a larger, profitable operator of a 66-satellite global network — and in doing so, recast itself from a launch provider into a fully vertically integrated space power. Founder Sir Peter Beck framed it bluntly: the combined company would become "a fully integrated self-launching space superpower." It is, for now, the boldest bet in commercial space outside of SpaceX.

What Rocket Lab Is Buying — and for How Much

Under the agreement, Rocket Lab will acquire all outstanding Iridium shares for $54.00 each, valuing Iridium at an enterprise value of approximately $8.0 billion. The offer is a cash-and-stock structure: $27.00 per share in cash, with the remainder paid in Rocket Lab stock subject to a collar that protects both sides against extreme swings in Rocket Lab's share price. The $54 figure represented roughly a 24% premium over Iridium's closing price on June 26, the last trading day before the announcement — and the market reaction was immediate, with Iridium shares jumping and Rocket Lab's own stock rising on the news.

The financial contrast between buyer and target is striking. In fiscal 2025, Iridium generated $871.7 million in revenue, about $495 million in operational EBITDA (a 57% margin), and $114.4 million in net income. Rocket Lab, by comparison, reported $601.8 million in revenue and a $198.2 million net loss over the same period — a smaller, still-unprofitable company acquiring a larger, cash-generating one. To fund the cash portion, Rocket Lab lined up a $3.6 billion bridge loan from Deutsche Bank and Wells Fargo, alongside balance-sheet cash and a mix of debt and equity financing. Chief Financial Officer Adam Spice called the transaction "significantly accretive" to cash flow and profitability, arguing it would materially transform Rocket Lab's financial profile. The deal is expected to close in mid-2027, pending approval from Iridium stockholders and regulators.

Why Iridium's L-Band Spectrum Is the Real Prize

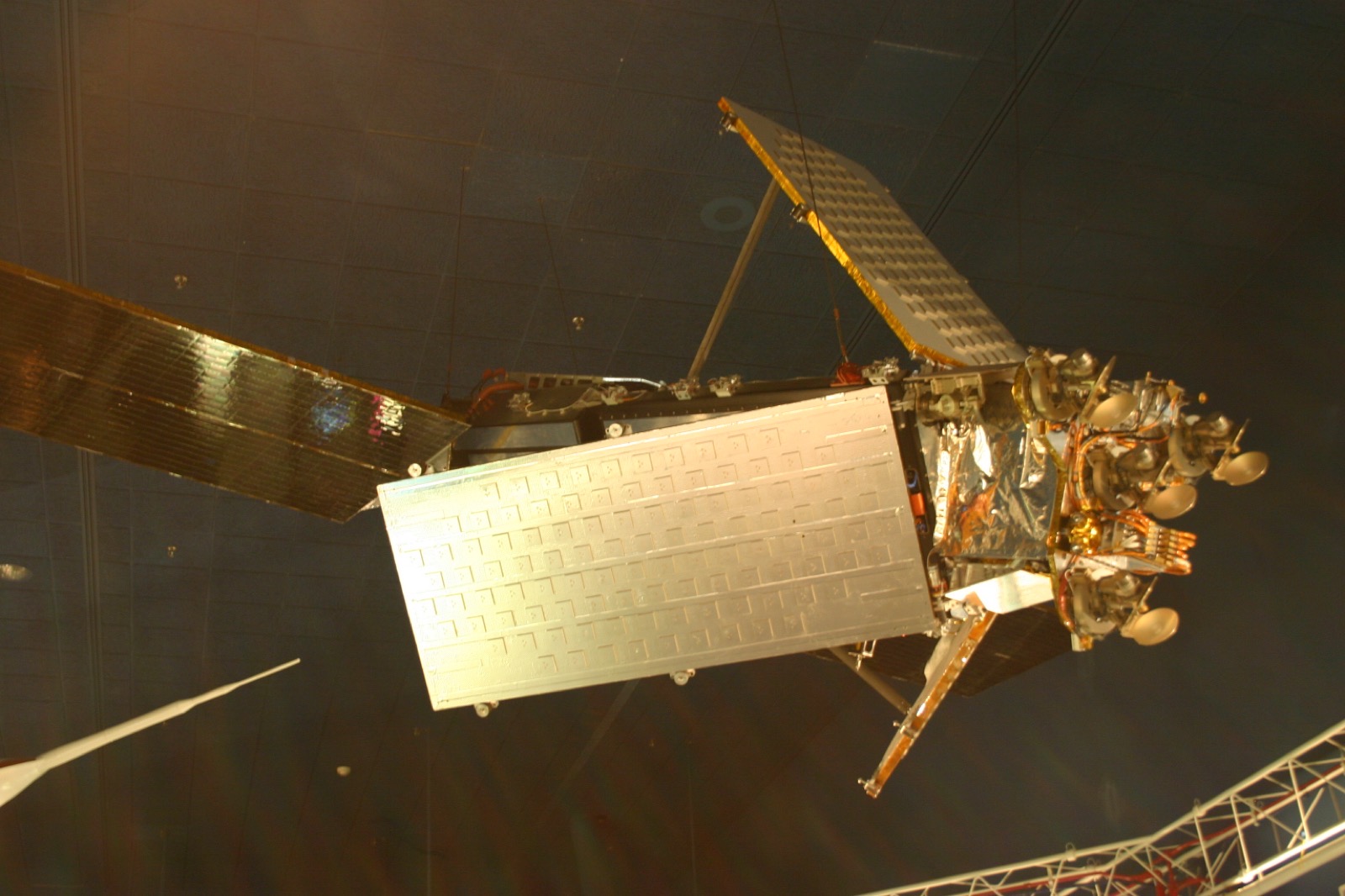

The headline asset is Iridium's constellation: 66 active satellites in low Earth orbit, plus in-orbit spares, arranged in six orbital planes that deliver true pole-to-pole coverage. What makes the network unusual is its cross-links — each satellite talks directly to its neighbors, so a signal can be routed across the globe without depending on a dense web of ground stations. That architecture, expensive and difficult to replicate, is why Iridium serves more than 2.55 million subscribers across government, defense, aviation, maritime, and remote industrial markets through an ecosystem of over 500 partner companies.

But the deeper prize is spectrum. Iridium holds globally coordinated L-band frequencies — a rare and jealously guarded resource that takes years and international negotiation to assemble. Beck had told investors in earlier earnings calls that he wanted Rocket Lab to eventually fly its own constellation, while conceding that the hardest parts were not the rockets or the satellites but securing globally harmonized spectrum and a paying customer base. Buying Iridium is the shortcut around both obstacles at once. The spectrum also opens doors Rocket Lab could not have built alone: direct-to-device (D2D) connectivity that links ordinary phones straight to satellites, and resilient positioning, navigation, and timing services that can serve as a backup to GPS. For anyone tracking the broader satellite broadband and direct-to-device market, Iridium's spectrum portfolio is the kind of asset that almost never comes up for sale.

How Rocket Lab Grew From a Small Rocket Into an $8 Billion Buyer

The acquisition is not a sudden pivot so much as the capstone of a long campaign. Rocket Lab's Electron has now flown more than 75 missions for customers ranging from commercial operators to NASA, making it the second-most-launched American orbital rocket after SpaceX's Falcon 9, and the company says its production line can turn out a rocket roughly every 11 days. Its larger, reusable Neutron rocket — designed for medium-lift payloads and constellation deployment — is targeting a first flight in late 2026. That progression from Electron to Neutron is chronicled in detail in this Rocket Lab company deep dive, and it matters here because owning a bigger rocket is exactly what a constellation operator needs to replenish aging satellites cheaply.

Alongside the rockets, Rocket Lab spent years quietly buying the pieces of a satellite. It absorbed Sinclair Interplanetary's spacecraft components in 2020, SolAero's space-grade solar cells in 2022, and Geost's electro-optical and infrared defense payloads in 2025. The pace accelerated through 2026 with a string of bolt-on deals — laser-communications specialist Mynaric, precision-component manufacturing, and space-robotics firm Motiv among them. Each purchase added a subsystem; together they turned Rocket Lab's Space Systems division into a business that now rivals its launch arm. Iridium completes the set in a way no component supplier could: it brings an operating network, the spectrum to run it, and recurring subscription revenue to help pay for everything else.

The Space Force Mission That Proved the Vertical-Integration Bet

If investors wanted proof that Rocket Lab could actually operate as a single integrated provider rather than a collection of acquisitions, they got it weeks before the Iridium announcement. In June 2026, Rocket Lab executed the U.S. Space Force's VICTUS HAZE tactically responsive space mission — and launched an Electron just 16 hours and 42 minutes after receiving the formal Notice to Launch from the Space Safari program office. That shattered the mission's 24-hour requirement and beat the previous responsive-launch record of 27 hours, set in 2023 during the VICTUS NOX demonstration flown by Firefly Aerospace.

What made VICTUS HAZE a milestone was not just the clock. Rocket Lab designed and built the maneuverable Pioneer spacecraft, integrated it, executed the rapid call-up launch, and is now operating the satellite on orbit — the first time a single prime contractor delivered an entire responsive-space mission as one end-to-end package. After reaching orbit, the company commissioned the spacecraft in 37 hours and 36 minutes, leaving it operational more than a day ahead of the 72-hour deadline. The demonstration was the vertical-integration thesis in miniature: design, build, launch, and operate, all under one roof. The Iridium deal simply scales that same idea from one responsive satellite to a 66-satellite global network.

What the Deal Means for the SpaceX–Rocket Lab Rivalry

For years, exactly one Western company has owned its rockets, built its satellites, and operated its own constellation: SpaceX, with Falcon and Starship lofting Starlink. That fully integrated loop is a large part of why SpaceX dominates the launch market and why investors hung such a premium on it when it went public — a story explored in this SpaceX investor deep dive. Rocket Lab's acquisition of Iridium is an explicit attempt to build a second instance of that model, at a smaller but still meaningful scale: Electron and Neutron for launch, an in-house manufacturing stack for the hardware, and Iridium for the network, spectrum, and customers.

The timing also fits a wider wave of consolidation. Just ten weeks earlier, in April 2026, Amazon agreed to acquire Iridium's longtime rival Globalstar for about $11.57 billion to power direct-to-device features for its Amazon Leo network — a deal that also folded in an Apple satellite-services partnership. With two of the three legacy mobile-satellite operators — Globalstar to Amazon, and now Iridium to Rocket Lab — being absorbed by larger players within months of each other, the era of standalone L- and S-band operators is closing fast. For Rocket Lab, the upside is strategic and financial at once: Iridium's steady subscription revenue gives it something Electron and Neutron never could on their own — a recurring cash engine to help fund the capital-hungry climb toward medium-lift reusability.

Risks, Regulators, and What Happens Before Mid-2027

None of this is guaranteed. The deal still needs a vote from Iridium stockholders and clearance from regulators, and a transfer of globally coordinated spectrum and a defense-adjacent satellite network will draw scrutiny from agencies overseeing foreign investment and communications licensing. Financially, layering a $3.6 billion bridge loan onto a company that is not yet profitable raises the stakes on integration: Rocket Lab must absorb a much larger operation without disrupting the subscriber base or the government contracts that make Iridium valuable. And there is a hardware clock ticking — the current Iridium NEXT constellation, deployed between 2017 and 2019 aboard SpaceX Falcon 9 rockets, will eventually need replenishment, which is precisely the job Neutron is meant to do. If Neutron slips badly, the economic logic of owning the constellation weakens.

Still, the strategic shape of the bet is clear. Iridium itself is a survivor — born inside Motorola in the 1990s, pushed into Chapter 11 bankruptcy in 1999, sold for just $25 million in 2001, and rebuilt into a profitable public company that today anchors critical communications for governments and industries worldwide. Pairing that resilient network with a launch company that just set a national responsive-space record is, as Beck put it, "a defining moment for the space industry." Iridium CEO Matt Desch echoed the logic, arguing that success now belongs to those who "can bring new innovations to space quickly and sustain them." If the transaction closes on schedule in mid-2027, Rocket Lab will emerge as only the second Western company to own every link in the chain from launch pad to subscriber — and the clearest structural challenger SpaceX has yet faced.