Space Companies

87 investor-grade profiles · 33 public · 54 private

Companies tracked

87

Public

33

Private

54

Countries

15

Most recent data verified 2026-06-12

Featured (anchor companies)

SpaceX

SPCX🇺🇸United StatesPublic

Launch & Satellite Internet

Reusable Falcon 9 booster fleet (individual cores 20+ flights) drives launch cost to $2,700–$3,200/kg to LEO — lowest globally. Vertically integrated supply chain. Starlink network effects with 10,000+ active sats and growing subscriber base provide recurring revenue that funds R&D.

Market Cap

~$1.77T (IPO price $135/share × 13.1B shares; intraday peak ~$2.2T on debut day 2026-06-12)

Employees

~13,000

Blue Origin

🇺🇸United StatesPrivate

Launch & Lunar Exploration

Effectively unlimited patient capital from Jeff Bezos. BE-4 engine is the sole powerplant for ULA Vulcan, creating a captive revenue stream. New Glenn's heavy-lift capability (45 t to LEO) directly competes with Falcon Heavy. Blue Moon Mk2 is NASA's second-sourced Artemis lander, providing government revenue anchor.

Valuation

$50B–$100B (industry estimates; no external funding)

Employees

~11,000

ULA

🇺🇸United StatesPrivate

National Security Launch

Dual-sourced NSSL certification gives ULA sole access alongside SpaceX to the most demanding national-security orbits. Vulcan Centaur's 27.2 t to LEO / 14.4 t to GTO capability fills the gap between Falcon 9 and Falcon Heavy. Decades of mission-assurance process maturity for classified payloads provide institutional trust.

Valuation

Not publicly disclosed (Boeing 50% + Lockheed Martin 50% joint venture)

Employees

~2,700

Sierra Space

🇺🇸United StatesPrivate

Spaceplanes & Commercial Stations

Dream Chaser is the only winged orbital spacecraft under development — enabling runway landing and return of sensitive or time-critical cargo that ballistic capsules cannot. LIFE inflatable habitat design is one of the most advanced commercial LEO habitat concepts. Orbital Reef partnership with Blue Origin creates a bundled station+transportation offering.

Valuation

$8B (post-money, Series C March 2026)

Employees

~2,000+

Series C · 2026-03-05

Axiom Space

🇺🇸United StatesPrivate

Commercial Space Stations

First-mover advantage in commercial ISS modules — Axiom Module 1 will be the first commercial hab on the station. Ex-NASA ISS program manager CEO brings unmatched operational credibility. AxEMU is the only next-gen US EVA spacesuit in development (replaces 40-year-old NASA EMUs). Ax-1 through Ax-4 provide flight heritage and NASA relationship capital.

Valuation

~$2.5B+ (PitchBook estimate post-Feb 2026 round)

Employees

~800+

Equity + Debt (mixed) · 2026-02-12

Vast

🇺🇸United StatesPrivate

Commercial Space Stations

Haven-1 is positioned to be the first standalone commercial space station in orbit if it holds its NET Q1 2027 launch date — it has NOT launched yet. Jed McCaleb's personal funding eliminates dilution pressure from institutional VCs. SpaceX partnership for both launch and crew transport removes dependency on rocket development. Lean team and Silicon Valley speed culture targeting faster iteration than defense-prime competitors.

Valuation

Undisclosed (no institutional VC rounds; Jed McCaleb primary funder)

Employees

~300+

Stoke Space

🇺🇸United StatesPrivate

Launch Vehicles

Full reusability of both stages (including upper stage — an unsolved industry problem) is Stoke's core technical moat. Hydrogen-fueled upper stage with full-flow staged combustion delivers high specific impulse. NSSL Lane 1 selection validates government confidence in the architecture. a16z Series C lead signals top-tier defense/space investor conviction. If Stoke achieves upper-stage reusability, it would be the first company to solve the problem SpaceX has not yet solved for Starship's Starship upper stage.

Valuation

Undisclosed (terms of the $860M Series D, Feb 2026, not disclosed)

Employees

~200+

Series D (extension) · 2026-02-10

Rocket Lab

RKLB🇺🇸United StatesPublic

Launch & Space Systems

Rocket Lab is the only publicly-traded company with both an operational dedicated small-launch vehicle and an in-house spacecraft manufacturing division, enabling end-to-end mission capability no other public new-space company can match. The $1.33B+ in SDA prime contracts validates its ability to serve as a Tier-1 defense prime. Its Photon spacecraft bus has flown to deep space (CAPSTONE; ESCAPADE); its components (RCS, separation systems, solar cells) have cumulative multi-hundred-mission heritage.

Market Cap

~$68.8B

Employees

~2,600+

Showing 87 of 87 companies · 8 featured above

Relativity Space

🇺🇸United StatesPrivate

3D-Printed Rockets

World's largest metal 3D printers (Stargate) enable rapid design iteration at a fraction of traditional tooling cost. Terran R's partially 3D-printed reusable first stage targets Falcon 9 payload class at lower per-unit manufacturing cost. SES anchor contract provides $200M+ revenue visibility.

Valuation

~$4.2B (post Series-E, 2023 — STALE: predates Eric Schmidt's 2025 controlling-stake investment, terms undisclosed)

Employees

~1,000

Varda Space Industries

🇺🇸United StatesPrivate

In-space manufacturing

First company to complete an end-to-end commercial in-space manufacturing mission (W-Series 1, 2024 — ritonavir crystal growth + reentry). Proprietary reentry capsule and manufacturing platform. Pharmacy-grade GMP in-space manufacturing is a regulatory moat; very few peers at this stage.

Valuation

Undisclosed post-Series C (July 2025)

Employees

~150

Series C · 2025-07

Northwood Space

🇺🇸United StatesPrivate

Ground Station as a Service (GSaaS)

Network effect: more ground stations enable higher contact frequency per orbit for a given satellite, which is the core product metric. Early USSF contract provides national-security credential and anchor revenue. a16z backing brings enterprise go-to-market expertise.

Valuation

~$136M total (incl. $100M Series B Jan 2026 + $49.8M USSF contract)

Employees

—

Series B · 2026-01-27

Intuitive Machines

LUNR🇺🇸United StatesPublic

Lunar Landing & Space Services

Intuitive Machines is the only company that has twice soft-landed spacecraft on the Moon commercially (IM-1 in Feb 2024 — first U.S. Moon landing since 1972; IM-2 in Mar 2025) and holds the largest single NASA contract ever awarded to the company ($4.82B NSN). The CLPS task order record (5 contracts, most of any provider) and the NSN anchor create an exceptionally durable government revenue relationship. The Lanteris Space Systems acquisition (closed Jan 13, 2026, $800M) expanded capabilities into orbital services.

Market Cap

~$5.1B

Employees

~525 (pre-Lanteris — STALE: excludes Lanteris Space Systems workforce added with the Jan 13, 2026 acquisition close; combined headcount not yet disclosed)

Virgin Galactic

SPCE🇺🇸United StatesPublic

Space Tourism

First-mover brand in commercial suborbital tourism with FAA commercial spaceflight license. Spaceport America in New Mexico provides exclusive operating base. Delta-class architecture targets ~10× the flight cadence of legacy VSS Unity, enabling unit economics that closed-cabin VSS Unity could not. Direct competition with Blue Origin's New Shepard remains the principal risk; Delta's higher cadence is the bet that differentiates the long-term cost curve.

Market Cap

~$120M

Employees

~750

Boeing

BA🇺🇸United StatesPublic

Aerospace & Human Spaceflight

Boeing retains a strong 702 satellite bus franchise (geostationary communications) and sole-source SLS core stage position for Artemis missions. However, its commercial crew competitive position has been severely damaged by Starliner failures, and its financial flexibility is constrained by $45B+ in net debt and ongoing 737 MAX production challenges.

Market Cap

$187B

Employees

~182,000

Astrobotic

🇺🇸United StatesPrivate

Lunar landers (CLPS)

First-mover position in CLPS — Peregrine Mission One was the maiden CLPS launch (Jan 2024). Griffin Mission 1 is the only confirmed cargo-class CLPS lander in the manifest. Years of NASA mission-design heritage from CMU spinoff roots.

Valuation

$380M

Employees

~250

Series C · 2024-11-20

Lunar Outpost

🇺🇸United StatesPrivate

Lunar mobility (LTV prime)

Lunar Dawn team includes Lockheed Martin, General Motors, Goodyear, and MDA Space — the most experienced industrial partnership of the three LTV primes. GM brings BEV powertrain heritage; Goodyear non-pneumatic tire IP.

Valuation

—

Employees

—

Venturi Astrolab

🇺🇸United StatesPrivate

Lunar mobility (LTV prime)

Only LTV prime that ALREADY has a flight manifest — FLIP rover flies on Griffin Mission 1 NET July 2026, years before the LTV down-select. Astrolab is also part-owned by Monaco's Venturi Group, which brings EV powertrain heritage.

Valuation

—

Employees

—

I

IX (Intuitive Machines + X-Energy)

🇺🇸United StatesPrivate

Lunar surface nuclear power

X-Energy brings TRISO fuel heritage (one of the few non-LEU US fuel forms with active reactor licensing under way). Intuitive Machines brings lunar surface mission integration experience from CLPS. Boeing + Maxar add space-systems heritage.

Valuation

—

Employees

—

Helios

🇮🇱IsraelPrivate

Lunar ISRU (oxygen + metal extraction)

Only company developing a unified molten-regolith-electrolysis pathway that yields BOTH oxygen and structural metals as co-products. Heritage from MIT-NASA Molten Oxide Electrolysis research dating to 2009.

Valuation

—

Employees

—

C

Crescent Space

🇺🇸United StatesPrivate

Lunar communications + navigation as a service

Backed by parent Lockheed Martin's spacecraft heritage (Lunar Trailblazer, Janus, GPS satellites). Uses Lockheed's existing Curio smallsat bus, derisking the constellation's spacecraft side.

Valuation

—

Employees

—

Draper

🇺🇸United StatesPrivate

Aerospace + defense R&D non-profit

Direct Apollo Guidance Computer heritage. Trusted by NASA for high-assurance G&N on crewed and high-value missions. Non-profit status removes shareholder pressure on long-horizon R&D.

Valuation

—

Employees

~2,000

Honeybee Robotics

🇺🇸United StatesPrivate

Space robotics + drilling systems

Decades-long heritage of flying space drilling hardware. Built the Perseverance rover's sample-caching drill and the TRIDENT drill for NASA's PRIME-1 ISRU demonstrator (flew on IM-2 March 2025). Now vertically integrated with Blue Origin for lunar surface ops.

Valuation

—

Employees

—

Collins Aerospace

🇺🇸United StatesPrivate

Space + defense systems

Heritage from the original Apollo + Shuttle EMU suit lineage via ILC Dover partnership. Team partners ILC Dover (Apollo suits) and Oceaneering (Shuttle EMU). One of only two providers selected under NASA's $3.5B xEVAS contract (the other is Axiom Space).

Valuation

—

Employees

—

Nokia Bell Labs

🇺🇸United StatesPublic

Telecommunications R&D

World's most established cellular R&D heritage — founded 1925 as the original Bell Telephone Laboratories. Reconceptualized Earth 4G/LTE for lunar conditions (vacuum, radiation, power-constrained), with first deployment on IM-2 March 2025.

Market Cap

—

Employees

—

Thales Alenia Space

🇫🇷FrancePublic

Space prime contractor

Decades of ESA pressurized-module heritage — built ATV, Cygnus pressurized modules, Cupola, and now Lunar Gateway HALO. Strongest European track record on crewed-rated pressurized vehicle structures.

Market Cap

—

Employees

—

Mitsubishi Electric

6503🇯🇵JapanPublic

Industrial electronics + space systems

Heritage as JAXA's primary prime contractor for satellite + spacecraft electronics. Built and operated SLIM, Japan's first lunar lander — successful precision landing January 2024 made Japan the 5th nation to soft-land on the Moon.

Market Cap

—

Employees

—

Toyota Motor Corporation

7203🇯🇵JapanPublic

Automotive manufacturing

Decades of fuel-cell (FCEV) commercialization heritage — Mirai is the world's first mass-produced hydrogen fuel-cell sedan. That FCEV technology is the architectural basis for Lunar Cruiser's 10-year mission endurance.

Market Cap

—

Employees

—

Westinghouse Electric Company

🇺🇸United StatesPrivate

Nuclear power systems

Patent portfolio + manufacturing capability across the commercial nuclear stack. eVinci microreactor design is one of the few US-developed micro-reactor concepts with both terrestrial deployment plans (Idaho National Lab demonstration 2026) and space-adapted variants.

Valuation

—

Employees

—

China Academy of Space Technology (CAST)

🇨🇳ChinaPrivate

State-owned space prime

Sole prime for all major Chinese lunar exploration missions. Direct heritage from Chang'e 1 through Chang'e 7 — accumulated lunar mission integration experience comparable only to NASA Goddard / JPL.

Valuation

—

Employees

—

Orienspace

🇨🇳ChinaPrivate

Sea-launched Solid Orbital Launch (China)

Only Chinese private operator with a flying sea-launched orbital rocket — Gravity-1's January 2024 debut delivered three satellites and set the world record for most powerful solid-propellant orbital vehicle. Sea-launch capability gives Orienspace operational flexibility no land-only Chinese private peer can match, and the Yantai/Shandong base location places it close to the active commercial sea-launch ecosystem also used by Galactic Energy's Ceres-1 and Deep Blue's Nebula-1. Founder Yao Song was a co-founder of AI-chip startup DeePhi Tech (acquired by Xilinx in 2018), bringing engineering and venture credibility to the launch program.

Valuation

Not publicly disclosed; trade-press estimates place it in the ~$700–850M range as of late 2024 following Series A and pre-A rounds

Employees

Not publicly disclosed

BlackSky Technology

BKSY🇺🇸United StatesPublic

Geospatial Intelligence

BlackSky's Gen-3 satellites deliver 35cm imagery resolution with rapid revisit — comparable to Planet's Pelican on resolution but with higher tasking responsiveness. The vertically-integrated stack (satellite + ground + AI software) lets BlackSky bundle Spectra AI analytics into imagery contracts, raising switching costs. NRO EOCL designation is a binary regulatory moat — only three commercial providers (BlackSky, Maxar, Planet) sit on the EOCL contract. International revenue mix (~50%) provides diversification away from U.S. budget cycles and is a deliberate hedge against EOCL renegotiation risk.

Market Cap

~$650M

Employees

~290

Iridium Communications

IRDM🇺🇸United StatesPublic

Satellite Communications

Iridium is the only L-band LEO constellation offering true global pole-to-pole coverage — a binary regulatory and physical moat. The 66-satellite cross-linked architecture is unique: Iridium satellites talk to each other in space, eliminating the need for a global ground-station network. The DoD EMSS unlimited-use contract is structurally sticky — it embeds Iridium across U.S. and allied military communications gear. L-band is the reliability standard for safety-of-life maritime and aviation services that Starlink LEO Ku-band cannot displace. Constellation fully paid for, no major capex until ~2030, supports double-digit free cash flow yield.

Market Cap

~$3.0B

Employees

~975

Kratos Defense

KTOS🇺🇸United StatesPublic

Defense Technology

Kratos differentiates as the 'disruptive prime' — sub-prime in size yet primary contract holder on critical DoD programs. Three durable advantages: (1) OpenSpace is the leading software-defined satellite ground system, achieving full virtualization in early 2026 — moves operators off proprietary hardware and creates platform lock-in; (2) Zeus 1/Zeus 2 solid rocket motors via L3Harris partnership give Kratos a unique position in hypersonic propulsion just as MACH-TB 2.0 ramps; (3) attritable / low-cost mass philosophy (Valkyrie tactical drone) aligns with DoD's shift toward affordable mass — a structural advantage versus traditional primes whose cost structure cannot match.

Market Cap

~$13B

Employees

~3,800

Palantir Technologies

PLTR🇺🇸United StatesPublic

Defense AI & Data Analytics

Palantir's moat in space and defense rests on (1) two decades of accreditation work — Foundry/Gotham/AIP are deployed at the highest U.S. classification levels, a barrier that takes 5-10 years for newer entrants to replicate; (2) Maven Smart System designation as a 'system of record' for DoD AI/ML, locking Palantir into the U.S. defense AI infrastructure; (3) AIP's deep enterprise penetration (137% U.S. commercial revenue growth in Q4 2025) gives Palantir a flywheel of training data and use-case proliferation that competitors cannot match; (4) co-development on $185B Golden Dome program with Anduril positions Palantir as a non-traditional prime in next-decade missile defense.

Market Cap

~$340B

Employees

~3,800

Viasat Inc

VSAT🇺🇸United StatesPublic

Satellite Communications & Broadband

Viasat's moat rests on three pillars: (1) Inmarsat L-band global safety-of-life services — the only commercial provider authorized for GMDSS maritime distress and aviation cockpit ATC; (2) #1 share in commercial in-flight broadband on widebody aircraft via long-term airline contracts; (3) Defense & Advanced Technologies segment provides high-assurance encryption (Type 1) and cyber capabilities that take a decade to certify. The principal moat erosion vector is Starlink LEO latency advantage on consumer airline broadband — Viasat is countering with ViaSat-3 capacity (~10× per satellite vs. ViaSat-2) and multi-orbit (LEO+GEO) hybrid offerings. Heavy debt ($7.2B) and slower share growth in IFC remain the financial overhang.

Market Cap

~$1.2B

Employees

~7,300 (post-Inmarsat integration)

OHB SE

OHB🇩🇪GermanyPublic

Satellite Manufacturing

Europe's largest independent satellite manufacturer and the only family-controlled tier-1 European space prime, behind Airbus Defence & Space and Thales Alenia Space in scale but ahead of every other independent. Sole-source heritage on Galileo (prime for 34 first-generation satellites), Hera (planetary defense), JUICE platform contributions and the Heinrich Hertz GEO demonstrator gives OHB a workshare floor on every flagship ESA mission. Bremen consolidates manufacturing, MGSE, AIT facilities and a dedicated cleanroom complex used by no other German prime.

Market Cap

~€5.0B (May 2026, share price ~€278)

Employees

~3,800 (Group, FY2025)

Eutelsat Group

ETL🇫🇷FrancePublic

Satellite Connectivity (GEO + LEO)

Eutelsat is the only operator on Earth running a fully-deployed multi-orbit (GEO + LEO) network at commercial scale. The 648-satellite OneWeb constellation is one of just two operational global LEO broadband networks (versus Starlink). UK Government is a strategic shareholder (10.89% post-2025 raise) with veto rights, anchoring sovereign UK demand, and Eutelsat is the anchor industrial partner inside the SpaceRISE consortium that won the EU's €10.6B IRIS² sovereign-connectivity concession through 2030. Spectrum holdings — Ku-band GEO across EMEA plus LEO Ku/Ka — and a 35-satellite GEO fleet provide a moat that no European competitor can replicate, although Starlink's pricing and scale remain the binding competitive constraint.

Market Cap

~€3.5B (May 2026, ETL.PA ~€2.96)

Employees

~1,800 (Group, post-merger)

Mynaric

🇩🇪GermanyPrivate

Laser Communications Terminals

World's only independent merchant supplier of production-volume optical inter-satellite link (OISL) terminals at SDA-mandated standards — competes with vertically captive Tesat-Spacecom (Airbus) and CACI's SA Photonics. Inherited 15+ years of DLR free-space optical research via 2009 spin-out. CONDOR Mk3 is qualified under SDA's Optical Communications Terminal Standard v3.0 — a moat because every Tranche 1/2/3 transport-layer satellite must carry interoperable terminals. Post-Rocket Lab acquisition, Mynaric gains the capital backing of a $20B+ market-cap parent, removes the going-concern overhang, and benefits from in-house demand on Rocket Lab's $1.3B Tranche 2 satellite primes. Manufacturing footprint in Munich (terminal assembly) and Los Angeles (final integration). Weakness: production-scaling track record is poor — repeated 2024 guidance cuts and delivery slips drove the StaRUG restructuring.

Valuation

—

Employees

~350 (Munich, Los Angeles, Washington D.C.)

Isar Aerospace

🇩🇪GermanyPrivate

European Small-Satellite Launch

First-mover advantage as the only fully private European launcher to attempt an orbital flight from continental Europe — Spectrum lifted off from Andøya on 30 March 2025 (first orbital test flight from mainland Europe) and is preparing the qualifying second flight 'Onward and Upward'. Vertically integrated production (~95% in-house manufacturing in Ottobrunn including 3D-printed Aquila LOX/propane engines), a private launch site agreement with Andøya Space, and the political backing of the German federal microlauncher policy make Isar the de-facto European national-champion launcher. Total financing of ~€870M (after the June 2026 €270M Series D) is the largest of any European launch startup and 3–5x deeper than nearest competitors RFA and PLD Space. LOX/propane propellant choice (cleaner-burning, denser than methane) is differentiated. Moat is real but contingent: it evaporates if the second flight fails or if RFA reaches orbit first.

Valuation

Over €1B (unicorn status confirmed July 2025 following Eldridge €150M convertible bond)

Employees

~430 (Ottobrunn HQ, plus Andøya launch operations)

Series D · 2026-06-09

PLD Space

🇪🇸SpainPrivate

European Launch

First — and to date only — Spanish company to have successfully flown a privately developed rocket (MIURA 1, Oct 2023). In-house liquid-engine and stage-recovery IP, anchored by Spain's CDTI/SEPI industrial backing and ESA's €169M ELC commitment, gives sovereign-launch credibility that pure commercial rivals lack. Mitsubishi Electric's strategic equity + launch-services agreement opens the Asian smallsat market and validates MIURA 5 commercially before first flight.

Valuation

Undisclosed (post-money post €180M Series C, Mar 2026)

Employees

~250 (post-Series C scale-up)

Series C · 2026-03-04

Rocket Factory Augsburg (RFA)

🇩🇪GermanyPrivate

European Launch

Only European new-space company building an oxygen-rich staged-combustion engine (Helix) — a higher-performance cycle than the gas-generator engines used by Isar's Aquila or Rocket Lab's Rutherford. Vertical integration (engine, stages, avionics) is reinforced by Aerospace Propulsion Products heritage. OHB SE's strategic shareholding gives an anchor European prime customer for payload integration. SaxaVord launch-pad exclusivity for the inaugural campaign and selection as anchor for the UK's first vertical orbital launch creates UK government alignment that competitors lack.

Valuation

Undisclosed; OHB SE strategic stake + KKR convertible (€30M, Aug 2023)

Employees

~400 (post-overhaul, ahead of inaugural flight)

Convertible bond (strategic) · 2023-08-08

T

TRL Space

🇨🇿Czech RepublicPrivate

Earth Observation & Space Science

Only Czech company to act as ESA prime contractor for two independent exploratory lunar missions (LUMI and LUGO), a distinction unprecedented in Central/Eastern Europe. TROLL's onboard AI (Zaitra-built) and Corac cybersecurity layer create a vertically integrated stack that competitors cannot easily replicate. Petr Kapoun chairs the Brno Space Cluster, giving preferred access to the region's 1,000+ space engineers. The 10% regional chamber equity stake provides institutional continuity and public procurement access.

Valuation

ESA contract funding for LUGO Pre-Phase A and LUMI Phase A/B; exact cumulative contract value undisclosed. Partial state backing: Brno Regional Chamber of Commerce holds ~10% equity stake

Employees

~30–50 across TRL Space plus sister companies Zaitra (AI/ML) and Corac Engineering (cybersecurity); Brno HQ plus branch in Kigali, Rwanda

Spacemanic

🇸🇰SlovakiaPrivate

Nanosatellite Manufacturing & Mission Integration

Spacemanic holds a unique position as the only company to have built Slovakia's entire national satellite fleet and is the go-to integrator for 'first national satellite' missions in Central/Eastern Europe. The ESA-funded CORVUS platform (1U–16U scalable bus) gives it a commercial product competitive with international platform vendors. CEO Jakub Kapuš sits on ESA's NewSpace Advisory Board to the Director General — direct institutional access to European funding programmes and procurement decisions. Having flown 8+ satellites across multiple launch vehicles (PSLV, Falcon 9, Ariane 6) by 2025 gives the company an operational track record that pre-flight competitors cannot match. Slovakia's 2022 ESA Associate Member status creates a structural pipeline of Slovak-funded space missions that Spacemanic is positioned to capture.

Valuation

ESA Pioneer Programme grant for CORVUS platform; no major venture capital round publicly disclosed. Revenue-funded through mission contracts and CubeSat hardware sales.

Employees

~23 full-time (per third-party company aggregators, 2025); expanded into larger Bratislava HQ in 2024

Skyroot Aerospace

🇮🇳IndiaPrivate

Private Launch (India)

First-mover in India's newly liberalized private launch market with a formal IN-SPACe authorization and a signed framework agreement giving Skyroot access to ISRO's Sriharikota launchpad and ground infrastructure. Proprietary 3D-printed solid, liquid, and cryogenic engines (Kalam and Raman series) achieve >90% indigenous content, materially reducing per-kg launch cost vs. global small-lift peers. India's labor cost base, a $160M war chest, and a unicorn brand pull top engineering talent that smaller global rivals struggle to retain.

Valuation

$1.1B (Series D unicorn round, post-money)

Employees

~537

Series D · 2026-05-07

Agnikul Cosmos

🇮🇳IndiaPrivate

3D-Printed Small-Lift Launch

Agnikul is the only company in the world to have flown a single-piece 3D-printed semi-cryogenic engine, validated on the Agnibaan SOrTeD mission (May 30, 2024). Its in-house Rocket Factory-1 can print a complete Agnilet engine in roughly 72 hours, collapsing the propulsion supply chain that takes traditional rivals 6-12 months. Agnikul also operates India's first and only private launchpad and mission control complex (ALP / AMC) at Sriharikota — built with ISRO support and exclusive to Agnikul under its IN-SPACe authorization, a regulatory and infrastructure moat that is effectively unrepeatable.

Valuation

$500M+ (Series C extension, post-money)

Employees

~250

Series C extension · 2025-11-22

Pixxel

🇮🇳IndiaPrivate

Hyperspectral Earth Observation

Pixxel operates the highest-resolution commercial hyperspectral satellites ever flown — 5 m GSD with 150+ contiguous bands — a step-change versus Planet Labs' multispectral Doves (3-5 m, 8 bands) and BlackSky's panchromatic high-revisit fleet. Hyperspectral data unlocks chemistry-level insights (crop disease, mineral signatures, methane leaks, water quality) that conventional EO cannot resolve, creating a defensible analytic moat. NASA CSDA selection plus Google as a strategic investor and customer give Pixxel a discoverability advantage in the U.S. government and enterprise data markets that Indian peers cannot easily replicate.

Valuation

~$210M (Series B post-money, pre-2026 extension)

Employees

~169

Series B Extension · 2024-12-09

Bellatrix Aerospace

🇮🇳IndiaPrivate

In-Space Propulsion

Bellatrix is the only Indian private company with both electric (Hall-effect) and green chemical propulsion qualified in space, demonstrated on POEM-3 and POEM-4 — a moat no other Indian peer holds. RUDRA is India's first non-toxic hydrazine replacement (HPGP), aligning with the global regulatory shift away from hydrazine and giving Bellatrix an export advantage as European and US satellite operators are forced off legacy fuels. The Pushpak OTV contract with NSIL positions Bellatrix as the sole Indian provider of last-mile orbital delivery — a high-margin service category dominated globally by Impulse Space and D-Orbit.

Valuation

~$31M cumulative

Employees

~90 (India), targeting ~115 EOY 2026 + up to 6 US-based

Pre-Series B · 2026-03-27

Dhruva Space

🇮🇳IndiaPrivate

Satellite Manufacturing & Mission Services

Dhruva Space is the only Indian private company with a flight-proven, end-to-end satellite mission stack — satellite bus, payload integration, NSIL launch brokerage, and ground operations — and it built the first private Indian satellite (Thybolt) launched on a PSLV. The deep working relationship with ISRO/NSIL, plus a government-recognized indigenous solar array program with the Technology Development Board, makes Dhruva the default 'Indian private prime' for foreign payload owners who want PSLV access at Indian cost economics. The company's vertically integrated platforms (satellite + integration + ground) compress lead times to under 12 months — a significant advantage over fragmented global rideshare players.

Valuation

$21.4M cumulative

Employees

200+

Pre-Series B (extending) · 2026-03-15

G

GalaxEye

🇮🇳IndiaPrivate

Multi-Sensor Earth Observation

GalaxEye is the world's first commercial company to fly a satellite that co-locates SAR and multispectral optical sensors on a single platform, enabling simultaneous all-weather radar plus high-resolution color imaging of the same scene — a capability that no peer (Capella, ICEYE, Umbra on the SAR side; Planet, BlackSky on the optical side) currently offers. This OptoSAR fusion produces data products impossible with either sensor alone — for example, vessel-detection-with-classification in cloudy maritime regions, or crop-stress maps that combine moisture (SAR) with chlorophyll (optical). With Mission Drishti operational since May 2026 and a defense-grade go-to-market through Indian and international agencies, GalaxEye has a several-year structural lead in fused EO.

Valuation

$18.8M cumulative

Employees

~105

Series A extension · 2026-03-12

D

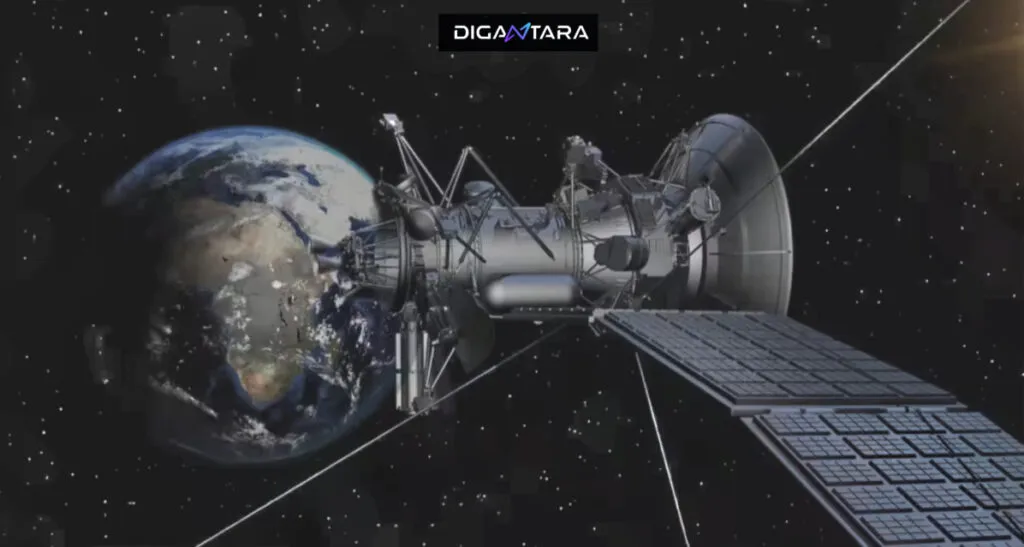

Digantara

🇮🇳IndiaPrivate

Space Situational Awareness (SSA)

Digantara owns the world's first commercial space-based SSA satellite (SCOT, launched January 2025) — a space-to-space optical tracker that detects RSOs as small as 5 cm in LEO, well below the 10 cm threshold of most ground-based catalogs. India's first dedicated SSA observatory in Garhwal Himalayas plus Asia's only commercial command-and-control center for space surveillance create a vertically integrated stack that no other Indian or APAC-region player matches. The pivot into space-based missile-warning extends the moat into a sovereign-defense category that closely resembles SDA Tracking Layer demand profile, but at Indian cost economics.

Valuation

~$200M (Rs 1,740 Cr post-money)

Employees

~120

Series B · 2026-04-30

SatSure

🇮🇳IndiaPrivate

Earth Observation Analytics

SatSure has the deepest commercial customer footprint of any Indian EO analytics company — direct contracts with three of India's top-five banks plus major crop insurers, accumulated over seven years of underwriting model iteration on Indian smallholder farmland. The company processes one of the world's largest farm-level satellite analytics datasets for crop-loan underwriting, generating proprietary ground-truth data that compounds over time. As part of the IN-SPACe Pixxel-led EO PPP consortium (with Pixxel, Dhruva Space, and PierSight), SatSure also has privileged access to India's first fully indigenous commercial EO constellation, complementing its existing public-feed-plus-AI stack.

Valuation

$29.5M cumulative across 13 rounds

Employees

~176 (Tracxn) / ~134 (LinkedIn-derived)

Series B extension · 2025-09-03

M

Manastu Space

🇮🇳IndiaPrivate

Green Satellite Propulsion

MS289 — Manastu's proprietary hydrogen-peroxide blend — is one of only a handful of flight-qualified non-toxic monopropellants globally, alongside ECAPS LMP-103S (Sweden) and NASA's AF-M315E. Successful Vyom 2U in-orbit firing on PSLV-C60 POEM-4 in December 2024 lifted the system to TRL-8, making Manastu the only Indian company with a commercially flight-qualified green thruster — a multi-year head start as the EU REACH regulation and NASA Class IV restrictions accelerate the global hydrazine phase-out. DRDO's Technology Development Fund partnership and IIT Bombay origins anchor the indigenous-defense customer pipeline that's hard for foreign competitors to replicate inside India.

Valuation

$9.02M cumulative

Employees

~40

Series A extension · 2026-03-31

A

Azista BST Aerospace

🇮🇳IndiaPrivate

Satellite Manufacturing (India)

ABA operates the largest private satellite manufacturing facility in Asia (50-250 satellites/year nameplate capacity in 50-200 kg class) and is one of only three Indian firms selected for the IN-SPACe SBaaS satellite-bus program (Feb 2026), alongside Dhruva Space and Astrome. The Berlin Space Technologies stake brings German flight-heritage bus design (BST has flown 10+ smallsats globally) directly into the Indian supply chain — a tech-transfer moat that pure-domestic peers can't match without years of design iteration. Combined with Azista Industries' deep manufacturing roots in pharma and defense, ABA has the rarest combination in Indian space: real factory throughput, foreign technical heritage, and a state-backed customer pipeline.

Valuation

Indo-German JV — primarily strategic JV funding, not priced VC rounds (Seed $4.58M, 2020); INR 5 Cr IN-SPACe SBaaS grant (2026-02)

Employees

~55 (+25% YoY)

Kawa Space

🇮🇳IndiaPrivate

Earth Observation Data + Smallsat Platforms (India)

Kawa Space is one of the earliest Indian private EO companies (founded 2018) with a fully integrated 'satellite + platform + analytics' stack — most Indian peers either build hardware (Pixxel, GalaxEye, Dhruva) or sell analytics on third-party imagery (SatSure), but Kawa controls both layers. Its early backing from Paytm founder Vijay Shekhar Sharma and Speciale Invest gave it a brand and customer-access advantage in Indian financial services, and the AWS Space Accelerator participation (April 2023) plugged it into AWS Ground Station and global cloud distribution. The Kawa Platform's API-first delivery model is differentiated from the imagery-as-product approach used by most legacy EO providers.

Valuation

~$1.86M cumulative

Employees

~104 (down 12% YoY from Aug 2024)

No priced round disclosed since pre-2023 (last documented seed extension; AWS Space Accelerator cohort participation 2023-04 was non-dilutive credits + mentorship) · 2023-04

Ananth Technologies

🇮🇳IndiaPrivate

Space Electronics + Satellite Systems (India)

ATL's moat is unrepeatable in the Indian space ecosystem: 30+ years of ISRO flight heritage spanning the PSLV harness, GSLV / GSLV-Mk III subsystems, and satellite electronics flown on Chandrayaan-1/-2/-3, Mangalyaan, Aditya-L1, RISAT, INSAT-3DS, and SpaDeX. No other private Indian company has delivered subsystems to interplanetary missions or to India's Mars and lunar programs. ATL also operates dedicated satellite manufacturing and integration facilities near Bangalore — the only private cleanroom infrastructure in India qualified for full ISRO satellite AIT (assembly, integration, test). The December 2024 IN-SPACe selection as India's first private GSO communication-satellite operator gives ATL a first-mover regulatory moat — Ka-band ITU filings are a finite sovereign resource, and ATL's filing has been assigned for end-to-end commercial use.

Valuation

Bootstrapped/self-funded since 1992 (family-owned; no external VC). ₹3,000 Cr (~$360M) capex commitment for GSO satcom build — largest single private space capex in India outside launchers.

Employees

~1,500 (group, including engineers + technicians across Hyderabad, Bengaluru, Thiruvananthapuram)

Satellize (formerly Exseed Space)

🇮🇳IndiaPrivate

Small Satellite / CubeSat Communications

First-mover credibility — Exseed built and launched India's first privately owned satellite (ExseedSAT-1, December 2018) before any private launch licensing framework existed. The company demonstrated it could go from contract to delivery in days (ExseedSAT-2 / AISAT was assembled in roughly six working days for AMSAT India), giving it operational know-how that newer Indian small-sat startups still have to acquire. Limited capital, however, means this moat is narrow versus better-funded peers like Dhruva Space or GalaxEye.

Valuation

~$316K (disclosed)

Employees

~391 (Tracxn — likely includes contract manufacturing/integration staff at Mumbai facility)

S

SkyServe

🇮🇳IndiaPrivate

In-Orbit Edge Computing

SkyServe is one of the only India-headquartered teams shipping a flight-validated edge-AI stack onto third-party satellites — the company has demonstrated multi-mission deployments with D-Orbit including the K2, Denali and Matterhorn missions, and has put its STORM platform through joint AI model evaluations with NASA JPL. That gives it an integrator-friendly position: an EO startup can plug SkyServe in instead of building its own onboard compute. Competing global edge-AI plays (Ubotica, Unibap) are well-funded but not Indian-licensed, so SkyServe also benefits from an IN-SPACe-aligned domestic pipeline.

Valuation

~$9M cumulative

Employees

~9-15 (Tracxn 9 / Crunchbase 15)

Seed (most recent disclosed; no Series A announced as of 2026-05) · 2023-09-27

satsearch

🇳🇱NetherlandsPrivate

Space Supply-Chain Marketplace

satsearch enjoys two-sided network effects: thousands of suppliers list their products to be discoverable, and engineers come to the platform because the supplier breadth is unmatched. ESA endorsement via the BIC Noordwijk programme adds institutional credibility that competing marketplaces struggle to replicate. The team's deep India presence — through co-founder Narayan Prasad and his Spaceport SARABHAI think tank — also positions satsearch as the default global-discovery layer for India's rapidly expanding post-IN-SPACe supplier ecosystem.

Valuation

Undisclosed; accelerator/grant capital + supplier subscription revenue

Employees

~20-40 (estimated)

LandSpace

🇨🇳ChinaPrivate

Methalox Launch (China)

First-mover and only proven Chinese commercial methalox orbital provider — Zhuque-2 beat SpaceX Starship, Blue Origin New Glenn, ULA Vulcan, and Relativity Terran R to first methane orbit in July 2023, building three-plus years of integrated propulsion, vehicle, and ground-ops experience that no Chinese rival has matched. Vertically integrated TQ-12/TQ-15A engine production at Huzhou and stainless-steel Zhuque-3 tank manufacturing at Jiaxing give LandSpace cost and IP advantages over peers reliant on third-party engines. State endorsement via the 900M-yuan Manufacturing Fund and STAR Market IPO counseling signals Beijing's preference for LandSpace as a national reusable-launch champion.

Valuation

~CNY 30B (~$4.1B) implied by July 2025 STAR Market IPO filing seeking CNY 7.5B raise

Employees

~1,000+ (Beijing HQ + Huzhou propulsion + Jiaxing manufacturing campuses)

Strategic state-backed (pre-IPO) · 2024-12

Galactic Energy

🇨🇳ChinaPrivate

Small + Medium Launch (China)

Ceres-1 is the most-flown Chinese private orbital rocket — 17 successful flights and over 70 satellites delivered by 2025 — giving Galactic Energy a flight-heritage and reliability moat that no other Chinese private operator can match. Proprietary solid-motor and kerolox engine production at the Chizhou propulsion campus, plus a dedicated sea-launch capability from Haiyang demonstrated in May 2024, broadens the operational envelope and reduces dependence on Jiuquan/Wenchang slot allocations. The CNY 2.4B Series D in September 2025 is one of the largest disclosed Chinese commercial-launch rounds and funds parallel Pallas-1, Pallas-2, and Ceres-2 development.

Valuation

~CNY 15B (~$2.1B) implied by Series D round (Sep 2025); pre-IPO counseling in progress

Employees

~600 (Beijing HQ + Anhui Chizhou propulsion test site + Shandong Haiyang sea-launch base)

Series D · 2025-09

Space Pioneer

🇨🇳ChinaPrivate

Reusable Medium-Heavy Launch (China)

Founder/CEO Kang Yonglai is the former CTO of LandSpace, giving Space Pioneer the deepest kerolox engine and large-vehicle integration experience among Chinese private launch entrants. Tianlong-2's April 2023 maiden-flight orbital success — a global first for a privately developed kerolox rocket — anchors the company's technical credibility with Chinese state and commercial customers. The Zhangjiagang production base, financed by the October 2025 Pre-D + D round, is targeting 30 Tianlong-3s and 500 engines per year — a manufacturing scale unmatched by any other Chinese private launch firm and necessary to capture Guowang/Qianfan deployment volume. Backing from Meituan Dragonball, Legend Capital, and Chinese Academy of Sciences/Zhejiang University-aligned funds ties the company to deep capital and political support networks.

Valuation

Implied ~CNY 25B+ (~$3.5B) post-money following combined Pre-D + D rounds (Oct 2025); IPO counseling rumored

Employees

~700+ (Beijing HQ + Zhangjiagang Tianlong-3 production base + Gongyi/Yulin engine test sites)

Combined Pre-D + D · 2025-10

DB

Deep Blue Aerospace

🇨🇳ChinaPrivate

Reusable Launch (Kerolox)

Earliest mover among Chinese privates on propulsive vertical-landing demonstration, with successful Nebula-M VTVL hops in 2022 (10m and 100m) and a high-altitude ~1,000m attempt in September 2024 that succeeded on ascent. In-house Thunder-R engine production and a state-backed Taishan-led funding round provide a domestic supply chain insulated from US ITAR/export-control exposure.

Valuation

Not publicly disclosed; Series B-IV implied valuation roughly CNY 5–6B (~$700–850M)

Employees

~300 (per company disclosures and PitchBook profile)

Series B-IV · 2025-03-10

iSpace (Beijing Interstellar Glory Space Technology)

🇨🇳ChinaPrivate

Reusable Launch (Methalox)

First-mover advantage as the only Chinese private firm to have reached orbit (Hyperbola-1, 2019), giving multi-year operational data others lack. Vertically integrated methalox stack (JD-1 hop-test engine, JD-2 flight engine — all qualified by April 2026), proprietary Qinglan autonomous sea-recovery drone ship, and the largest single funding round in Chinese private aerospace history (CNY 5.04B Feb 2026) provide capital and infrastructure leadership relative to Chinese reusable-rocket peers.

Valuation

Post-money not disclosed; CNY 5.04B (~$730M) Series D++ Feb 2026 implies multi-billion-dollar valuation — analysts estimate ~$2–3B

Employees

~300–400 (per industry analyst databases including PitchBook and Tracxn)

Series D++ · 2026-02-09

E

ExPace (Expace Technology / CASIC Rocket Technology)

🇨🇳ChinaPrivate

Solid-Fuel Small/Medium Launch (Quick-Reaction)

Sole CASIC commercial launch arm with 30+ Kuaizhou-1A flights and ~90% success rate as of late 2025 — the most-flown Chinese commercial launcher by mission count. Vertically integrated solid motor production (CASIC Fourth Academy heritage from DF-21 / DF-26 missile families), dedicated 68.8 sq-km Wuhan industrial base, and direct access to CASIC parent military launch demand insulate ExPace from the cash-burn pressures facing Chinese private launch peers. Lower per-mission pricing than CASC Long March on small payloads.

Valuation

State-owned CASIC subsidiary; cumulative external private capital ~$417M including $237M Series B (Jun 2022). Market valuation not publicly disclosed

Employees

~1,000+ at the Wuhan industrial base (per CASIC group disclosures)

Series B · 2022-06-14

G

GalaxySpace (Yinhe Hangtian)

🇨🇳ChinaPrivate

Satellite Manufacturing & LEO Broadband

Only private Chinese supplier qualified to deliver flat-panel stackable broadband satellites into Guowang batches, plus a 100-150 sat/yr smart factory in Nantong that no other domestic private peer has replicated. Q/V-band payload heritage from the original Yinhe-1/Mini-Spider Web demonstration plus an early lead in direct-to-handset NTN testing (first Chinese D2D handset call) gives it a one-to-two-year tech lead over LandSpace's spacecraft arm and CASIC's internal builders. A deep state-backed cap table (CCB, Hefei, Anhui) effectively guarantees domestic procurement allocation.

Valuation

~CNY 32B (~$4.5B) post-money — Series C close Feb 2025; A-share IPO counseling filed Mar 2026

Employees

~700

Series C (close) · 2025-02

CAS Space (Zhongke Aerospace Exploration / Zhongkexing)

🇨🇳ChinaPrivate

Launch (solid-fuel and reusable liquid rockets)

Direct affiliation with the Chinese Academy of Sciences gives CAS Space privileged access to CAS-developed propulsion, materials, and avionics IP — a moat no fully-private peer (LandSpace, Galactic Energy, Space Pioneer) enjoys. Kinetica-1 is the best-flown private Chinese launcher (12 orbital missions, ~92% success), and the company holds the dominant private launch market share in China. The early Kinetica-2 flight (Mar 2026) put it ahead of LandSpace's Zhuque-3 and Space Pioneer's Tianlong-3 on liquid medium-lift cadence, and the Qingzhou cargo-spacecraft pre-positions CAS Space for recurring CMSA revenue once Tianzhou is reduced.

Valuation

~CNY 11.1B (~$1.55-1.6B) per 2025 pre-IPO mark; targeting ~CNY 4.18B (~$607M) Shanghai STAR Market IPO raise

Employees

~600 (per 2025 IPO disclosures and trade-press reporting)

Pre-IPO strategic · 2025-08

Astroscale

186A🇯🇵JapanPublic

Orbital Debris Removal

Only company globally to have demonstrated commercial close-proximity operations with an uncooperative debris target (ADRAS-J, Nov 2024). Multi-jurisdiction footprint (Japan, UK, US, France) lets Astroscale win programs from JAXA, ESA, UK Space Agency, and USSF that single-country competitors cannot. Tokyo Growth Market listing (186A) provides public-market capital that private rivals like ClearSpace lack. Backlog of ~¥34B+ from ADRAS-J2 and ELSA-M provides multi-year revenue visibility into the operational service phase.

Market Cap

~¥120B (~$770M)

Employees

~480

ispace Inc

9348🇯🇵JapanPublic

Lunar Landers

First Japanese commercial lunar lander operator and the only lunar-pure-play company listed on a major Asian exchange (TSE: 9348). Two completed launches (Mission 1 in 2022, Mission 2 in January 2025) — both crashed but each generated paying customer revenue and proprietary trajectory/operations data unmatched by peers. Strategic alignment with JAXA, the UAE Rashid program, and NASA CLPS via the Draper-led contract gives ispace a multi-jurisdictional customer base. Competing directly with Intuitive Machines (NASDAQ: LUNR) and Firefly Aerospace's Blue Ghost.

Market Cap

~¥62B (~$400M)

Employees

~280

Korea Aerospace Industries (KAI)

047810🇰🇷South KoreaPublic

Aerospace Prime Contractor

Sole national aerospace prime in South Korea — monopoly position on KF-21, Surion, T-50 family, and primary contractor on Nuri/CAS500/Danuri. Three-decade institutional relationship with DAPA and KARI gives privileged access to ₩30T+ in defense and space programs. KOSPI listing (047810) provides public-market scale advantages over private competitors. Hanwha Aerospace is the only domestic peer with comparable propulsion and rocket capabilities, but KAI retains airframe, satellite-bus, and integration expertise. Growing T-50/FA-50 export wins (Poland, Malaysia, Egypt pipeline) diversify beyond domestic dependence.

Market Cap

~₩9.5T (~$7.0B)

Employees

~5,800

I

Innospace

462350🇰🇷South KoreaPublic

Small Satellite Launch

First publicly-traded South Korean space company (KOSDAQ: 462350, July 2024 IPO), giving it public-market capital access that domestic rival Perigee Aerospace lacks. Hybrid-propulsion architecture (paraffin fuel + liquid oxidizer) differentiates from kerosene/methane peers and offers safer ground-handling. Strategic launch-site partnership with Brazil's Alcântara Space Center provides equatorial launch advantage. KASA authorization for the SPACEWARD commercial campaign positions Innospace as Korea's authorized commercial launcher. The December 2025 failure pushes commercial service back, but the joint CENIPA investigation and rapid root-cause closure (March 2026) preserved customer relationships.

Market Cap

~₩175B (~$125M)

Employees

~140

C

Contec

451760🇰🇷South KoreaPublic

Ground-Station-as-a-Service

First-mover advantage as Korea's only KOSDAQ-listed GSaaS pure-play (451760, Nov 2023 IPO) with KARI heritage providing technical credibility. Operates 12 ground stations across 10 countries — among the largest independent GSaaS networks globally, competing with AWS Ground Station, KSAT, Viasat RTE, Atlas Space, and Leaf Space. Vertical integration into EO data pre-processing and analytics differentiates from pure-RF peers. Cailabs partnership for optical ground stations positions Contec as one of the few networks ready for the laser-comms transition. Q4 2025 first quarterly profit since listing demonstrates the infrastructure capex cycle is concluding and recurring-revenue monetization has begun.

Market Cap

~₩290B (~$210M)

Employees

~150

Telesat

TSAT🇨🇦CanadaPublic

Satellite Communications

Telesat's moat is partly its GEO fleet heritage (priority orbital slots, regulatory relationships, government anchor customer status in Canada) and partly the Lightspeed financing milestone — the CAD $2.54B combined federal+Quebec loan package effectively makes the Canadian government a strategic backer of the constellation. Lightspeed's optical inter-satellite links and four-terminal-per-satellite architecture are differentiated for enterprise/government users who need secure, sovereign alternatives to Starlink. The MDA manufacturing contract anchors a domestic supply chain. Risks: Telesat is competing with Starlink (8,000+ satellites operational), Eutelsat OneWeb (650+ satellites), and Amazon Kuiper at much smaller scale, and faces a critical 2026 debt-maturity wall with $1.7B coming due that auditors flagged as a going-concern risk.

Market Cap

~US$300M (depressed equity reflecting GEO decline and Lightspeed transition risk)

Employees

~600-1,000 (Telesat Canada ~610; consolidated headcount ~1,000 across 6 continents as of March 2026)

ImageSat International (ISI)

ISI🇮🇱IsraelPublic

Earth Observation

ISI is one of the very few independent commercial Earth-observation operators with sovereign-grade pedigree — its EROS satellites are built by IAI from heritage spy satellite designs, giving the imagery defense-grade quality and tasking flexibility that commercial peers like Planet Labs lack. Israeli national security relationships and ITAR-free status (relative to U.S. peers) allow ISI to serve customers in Asia, Africa, the Middle East, and Eastern Europe that Maxar and BlackSky cannot. The company's small focused fleet limits unit economics versus mass-deployment LEO peers, but the high revenue per satellite from defense customers ($42M two-year, $37.5M five-year deals) reflects the premium pricing of intelligence-grade imagery. The e-GEOS partnership adds SAR (radar) capability through Italian COSMO-SkyMed access for combined optical+radar offerings.

Market Cap

~US$225M (~NIS 815M)

Employees

~115

SIL

SpaceIL

🇮🇱IsraelPrivate

Lunar Exploration

SpaceIL's defining asset is the institutional knowledge of having actually built and flown a lunar lander to lunar orbit on a private budget — a feat shared by only a handful of organizations globally (ispace, Intuitive Machines, Firefly Aerospace). The nonprofit model and Israeli national pride attached to the program create a unique fundraising base that no commercial competitor has. The IAI engineering partnership brings sovereign-grade spacecraft heritage. However, the moat is currently dormant — without restored funding, SpaceIL cannot capitalize on Beresheet's hard-won engineering lessons, and ispace and Intuitive Machines are widening the lead in commercial lunar landing capability.

Valuation

Nonprofit organization; not for profit (Israeli public benefit company / 501(c)(3)-equivalent)

Employees

—

Akaer

🇧🇷BrazilPrivate

Space

Akaer's deepest moat is vertical integration of optical payload design through its Opto Space & Defense subsidiary — the only Brazilian entity capable of building satellite cameras end-to-end. This sovereign capability makes Akaer the mandatory Brazilian partner for any INPE or AEB optical mission, insulating it from foreign competition on domestic government contracts. The longstanding Saab partnership (28% stake, cross-JV equity in SAM) provides access to Gripen E aerostructures work that no other Brazilian independent integrator can replicate. A second location at the Bahia Aerospace Technology Park adds lower-cost manufacturing capacity.

Valuation

Undisclosed — privately held; Saab AB holds ~28% minority stake (stock-swap agreement, 2017). No external equity valuation published.

Employees

~350+ direct employees (group-wide, São José dos Campos + Bahia units)

D

Dragonfly Aerospace

🇿🇦South AfricaPrivate

Space

Dragonfly is one of fewer than a dozen companies globally capable of designing and manufacturing high-resolution multispectral EO payloads at scale outside the US/Europe/Israel axis. Its Stellenbosch location gives it access to South Africa's university-trained photonics and optical engineering talent at a cost structure well below Western counterparts. The Noosphere Ventures connection brings guaranteed anchor customer demand (EOSDA constellation) that de-risks R&D investment and provides an in-house proving ground for new imager variants. The SWIR product line expansion in 2024 opens new markets — methane/GHG monitoring, mineral exploration, agriculture — that are among the fastest-growing segments in commercial EO.

Valuation

Undisclosed — privately held, majority-owned by Noosphere Ventures (Max Polyakov). No funding amounts publicly disclosed.

Employees

~70–100 (PitchBook ~71 as of mid-2024; company states 100+ in CEO interviews)

NewSpace Systems

🇿🇦South AfricaPrivate

Space

NewSpace Systems' moat is rooted in three reinforcing factors: (1) Flight heritage — with 2,500+ spacecraft across 38 countries, its reaction wheels and sun sensors carry more orbital flight hours than most rivals, a critical differentiator for satellite constellation operators who cannot tolerate hardware failures at scale; (2) Scale economics — the new 5,200 sqm Somerset West factory with Helmholtz calibration zones, dark rooms, and thermal/vibration testing represents capital investment few competitors at this price point can match, enabling NSS to quote competitively on 500+ unit production runs; (3) Cost structure — ZAR-denominated manufacturing costs for USD/EUR-denominated contracts creates a persistent structural cost advantage over European GNC component manufacturers. This combination of certified quality, proven heritage, and low cost is difficult to replicate quickly.

Valuation

Undisclosed — privately held subsidiary of Schauenburg International (acquired January 2020). Annual revenue estimated at ~USD 5.6M (2025, third-party estimate); not officially confirmed.

Employees

~160 highly skilled professionals (group-wide, Somerset West HQ + US/UK/NZ offices)

Corporate Acquisition · 2020-01-29

AST SpaceMobile

ASTS🇺🇸United StatesPublic

Direct-to-Cell Satellite Broadband

AST SpaceMobile holds first-mover advantage in direct-to-device (unmodified smartphone) LEO broadband — a fundamentally different approach from SpaceX Starlink (which requires proprietary terminals). The partnership network of AT&T, Verizon, T-Mobile, Vodafone, Rakuten, and Google gives access to billions of existing subscribers without direct consumer acquisition costs. Its large-aperture BlueBird satellites are a proprietary design; the company has filed hundreds of IP patents on its array technology. The addressable market of 5.4B+ unconnected mobile users is orders of magnitude larger than the specialty broadband market.

Market Cap

~$22B

Employees

~1,800+

Redwire

RDW🇺🇸United StatesPublic

Space Infrastructure & Manufacturing

Redwire holds the only flight-proven roll-out solar array technology (ROSA) with a 100% on-orbit success rate across ISS, Gateway, and commercial satellites. iROSA delivered six pairs to the ISS, upgrading its power supply — a mission-critical sole-source position. Its in-space manufacturing and bioprinting capabilities address growing commercial station and on-orbit servicing markets.

Market Cap

~$1.7B

Employees

~1,410

Planet Labs

PL🇺🇸United StatesPublic

Earth Observation & Geospatial Analytics

Planet holds three overlapping moats: the world's most comprehensive EO data archive (daily global coverage since 2017 — no other commercial operator has this temporal depth); the lowest per-image cost at scale via CubeSat manufacturing; and deep integration into hundreds of government and commercial analytics workflows that create high switching costs. The $230M customer-funded Pelican contract and the $900M+ backlog reflect the durable, contract-based nature of the business.

Market Cap

~$12.8B

Employees

~970

Lockheed Martin

LMT🇺🇸United StatesPublic

Defense & Space Systems

Lockheed Martin holds sole-source positions on Orion (NASA Artemis), GPS III/IIIF, and Next-Gen OPIR — three flagship national-security and exploration programs where switching costs are prohibitive. With 124 SDA satellites on contract across three tranches, the company is the leading tracking-layer integrator in the Proliferated Warfighter Space Architecture.

Market Cap

$118.7B

Employees

~123,000

Northrop Grumman

NOC🇺🇸United StatesPublic

Defense & Space Infrastructure

Northrop Grumman is the sole provider of SLS solid rocket boosters, locking it into every NASA Artemis mission. As JWST prime contractor it holds 20+ years of follow-on science operations. The HALO module for the lunar Gateway represents a decade of crewed-station revenue. Decades of classified NRO satellite experience creates non-replicable institutional knowledge in the intelligence community.

Market Cap

$78.0B

Employees

~95,000

RTX Corp

RTX🇺🇸United StatesPublic

Defense & Aerospace Systems

RTX's Raytheon division is the dominant U.S. provider of space-based infrared missile-warning sensor payloads — its sensors fly on SBIRS, Next-Gen OPIR (as subcontractor to LMT), and HBTSS tracking satellites. The Pratt & Whitney RL10 upper-stage engine holds a near-monopoly on U.S. upper stages (Centaur V, ACES). Collins Aerospace avionics and space life-support systems fly on Orion and ISS.

Market Cap

$238B

Employees

~180,000

L3Harris Technologies

LHX🇺🇸United StatesPublic

Defense Sensors & Space Systems

L3Harris has won SDA Tracking Layer awards across every tranche (T0: 4 satellites, T1: 18, T2: 18, T3: 18 — 58 satellites total), making it the most embedded tracking-layer prime in the Proliferated Warfighter Space Architecture. Its classified NRO optical and RF sensor heritage is decades deep. NTS-3 positions L3Harris as the U.S. leader in experimental GPS augmentation.

Market Cap

$56B

Employees

~45,000

Voyager Technologies

VOYG🇺🇸United StatesPublic

Commercial Space Stations & Government Services

One of only two companies awarded NASA CLD Phase 2 contracts (alongside Axiom Space), giving Voyager Technologies a direct path to replacing the ISS. The Airbus and Northrop Grumman industrial partnerships bring heritage space station systems engineering and manufacturing scale. Government services segment provides current cash flows while Starlab development matures.

Market Cap

~$1.2B

Employees

~1,200+

Firefly Aerospace

FLY🇺🇸United StatesPublic

Launch & Lunar Services

Only company to have completed a fully successful commercial Moon soft-landing (Blue Ghost M1, March 2025). Multiple secured CLPS contracts totaling ~$450M provide government revenue anchor. Alpha rocket cadence growing with Air Force rideshare contracts. Northrop Grumman MLV partnership brings mission-assurance pedigree to medium-lift market.

Market Cap

~$5.2B

Employees

~1,200 (post-IPO + SciTec acquisition)

MDA Space

MDA🇨🇦CanadaPublic

Space Robotics & Satellite Manufacturing

MDA's Canadarm heritage is unmatched globally — 50+ years of continuous robotic arm operation on the Shuttle, ISS, and now Gateway creates a near-monopoly on crewed spacecraft robotic systems. The Canadarm3 contract ($2.65B total) anchors the company in NASA's Artemis program for the next 15+ years. Telesat Lightspeed manufacturing and SatixFy communications technology (acquired 2025) diversify revenue into the high-growth LEO constellation manufacturing market. The CHORUS SAR constellation provides owned Earth observation data revenue alongside manufacturing services.

Market Cap

~CAD $5.8B

Employees

~4,000